.svg)

The Industry Leader in Benefit Analytics for

Smarter benefits decisions start with better data. Benchmark, model, and measure your benefits against the market, instantly.

.png)

.png)

.svg)

When benefits are clear, everyone wins.

Whether you’re choosing, designing, selling, or managing benefits, we bring clarity and confidence to the process.

.svg)

.svg)

.svg)

.svg)

.svg)

Why Benefits Matter

3M+

Employers

offer healthcare and benefits to attract and support

their workforce.

160M+

Employees

in America rely on employer-

provided health and

benefits coverage.

$1.5T+

Invested

each year by employers towards employee health and benefits.

Solutions for Industry Leaders

Insights+ - Plan Rating

.svg)

Validate the strength of your benefits

Recruit and retain top-performing talent

Stand out in a competitive talent market

.png)

Insights - Benefits Benchmarking

Fast, presentation-ready reports

Trusted third-party market data

Comprehensive, micro-targeted insights

.png)

Catalyst - Market Analytics

Consult better with real-time market analytics

Organic growth solutions for leading advisors

One platform for benefits, PC & retirement

Supporting Benefit

Industry Leaders

Mployer is transforming employee benefits by delivering new levels of transparency in employee benefit plan design and market intelligence. By leveraging member-contributed data from across our ecosystem of employers, employees, brokers, carriers, and other service providers - enhanced with proprietary algorithms and advanced analytics - we empower leading insurance advisors and employers to reduce costs, boost engagement, and implement smarter strategies. The result: sustainable growth and better outcomes for everyone involved.

Mployer offers the largest, most comprehensive recurring benefits data asset in the industry - and we're growing daily.

Learn MoreWhat can we help

you achieve?

Our goal is a strong partnership focused on supporting your goals. Our products and roadmaps are customer driven. We build solutions to support industry-leading brokers and their employer clients. How can we support you?

.svg)

.svg)

Recent Market Trends

Understanding How Your Health Plan Is Funded Matters More Than Most Employers Think

How an employer funds its health plan sits quietly in the background of every benefits decision. Most CHROs and CFOs know their premium cost. Fewer understand the mechanics of how their plan is actually structured: who holds the risk, who administers the claims, how costs flow, and what flexibility, if any, they have to change any of it.

This post is not an argument for any particular funding model. It is an explanation of how each one works, what the national data shows about adoption by employer size, the key terms you need to understand, and the questions worth asking at your next renewal, whether you are fully insured today and want to stay that way, or whether you want to understand what moving to a different model would actually involve.

One important framing note upfront: funding model decisions are not one-size-fits-all. Fully insured arrangements are the right choice for a significant portion of employers, particularly smaller organizations, because the risk transfer and administrative simplicity is genuinely valuable. The goal here is clarity, not a prescription.

The Three Funding Models: What They Actually Mean

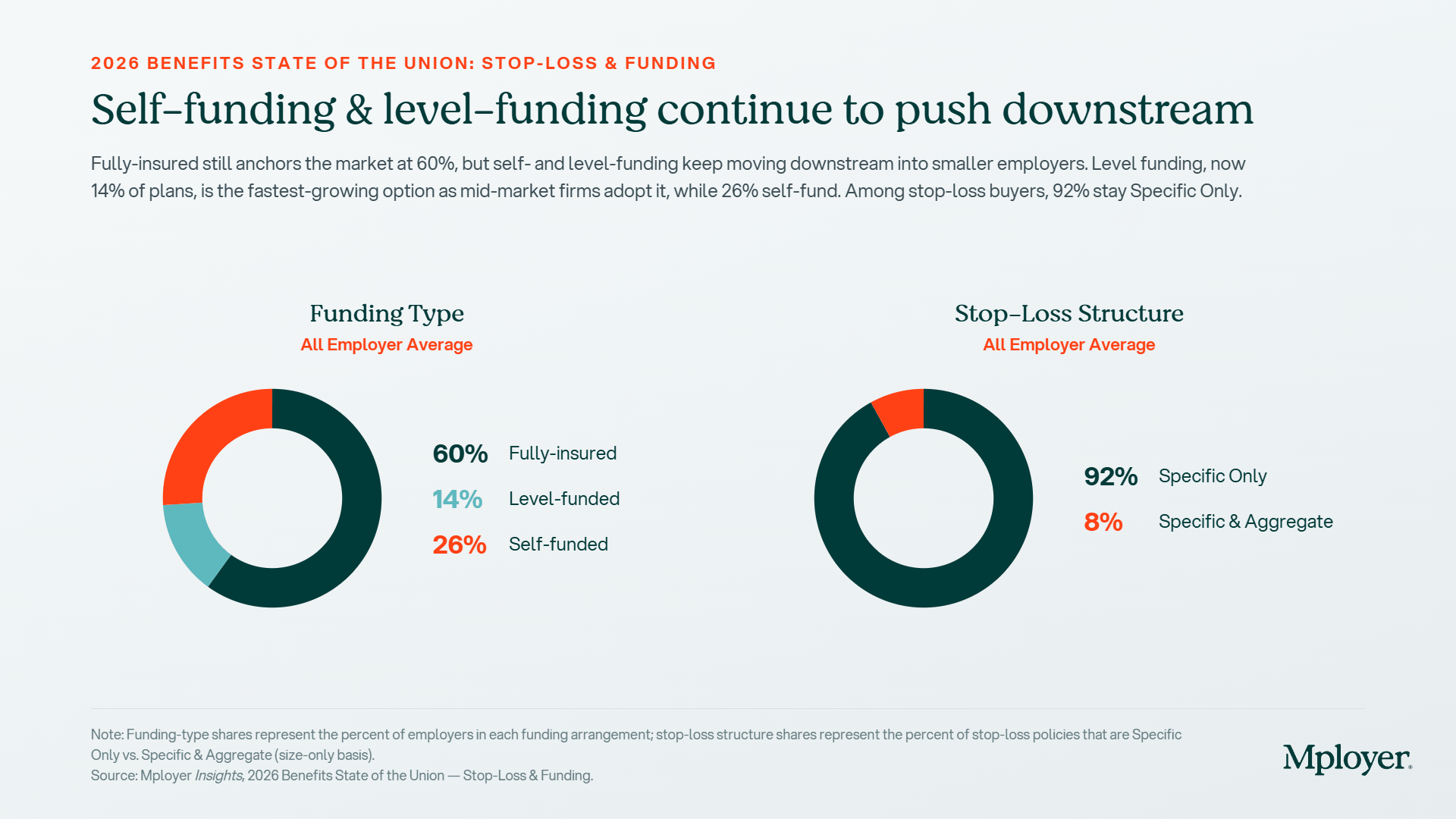

Nationally, 60% of employers are fully insured, 14% are level-funded, and 26% are self-funded, according to Mployer’s 2026 plan data covering 50,000+ employers. But those percentages look very different when you break them out by employer size. Among employers with fewer than 50 employees, fully insured is nearly universal while level-funded and self-funded require a minimum threshold of covered lives to be actuarially viable. The self-funded number rises sharply as employer size grows: roughly 27% of firms with 100–199 employees self-insure, compared to over 90% of firms with 5,000+ employees (DOL).

Fully Insured

The employer pays a fixed monthly premium to a carrier. The carrier assumes all financial risk for claims, manages the network, processes claims, and handles member services. The employer knows their cost in advance, there are no surprises if utilization spikes, but there is also no upside if the workforce has a healthy year. Premium increases at renewal are driven by the carrier’s projections, not the employer’s actual claims experience.

Per Member Per Month (PMPM) costs under fully insured arrangements include the carrier’s built-in risk margin and profit load, typically estimated at 10–15% of premium above what actual claims would cost. For a 200-person employer paying $700 PMPM in premium, that margin can represent $140,000–$210,000 per year in cost that never returns to the employer regardless of utilization. Fully insured is the right choice when an employer values predictability and simplicity above all else, or when their workforce is too small to absorb claims risk directly.

Level-Funded

Level-funded plans are the middle ground that has expanded significantly in the past decade, particularly for mid-size employers. The employer pays a fixed monthly amount, similar to a fully insured premium, but that payment is split into three components: a claims fund (to pay expected claims), a stop-loss premium (to cover catastrophic claims above a threshold), and an administrative fee. If actual claims come in below the funded level, the employer receives a refund of the surplus at year-end.

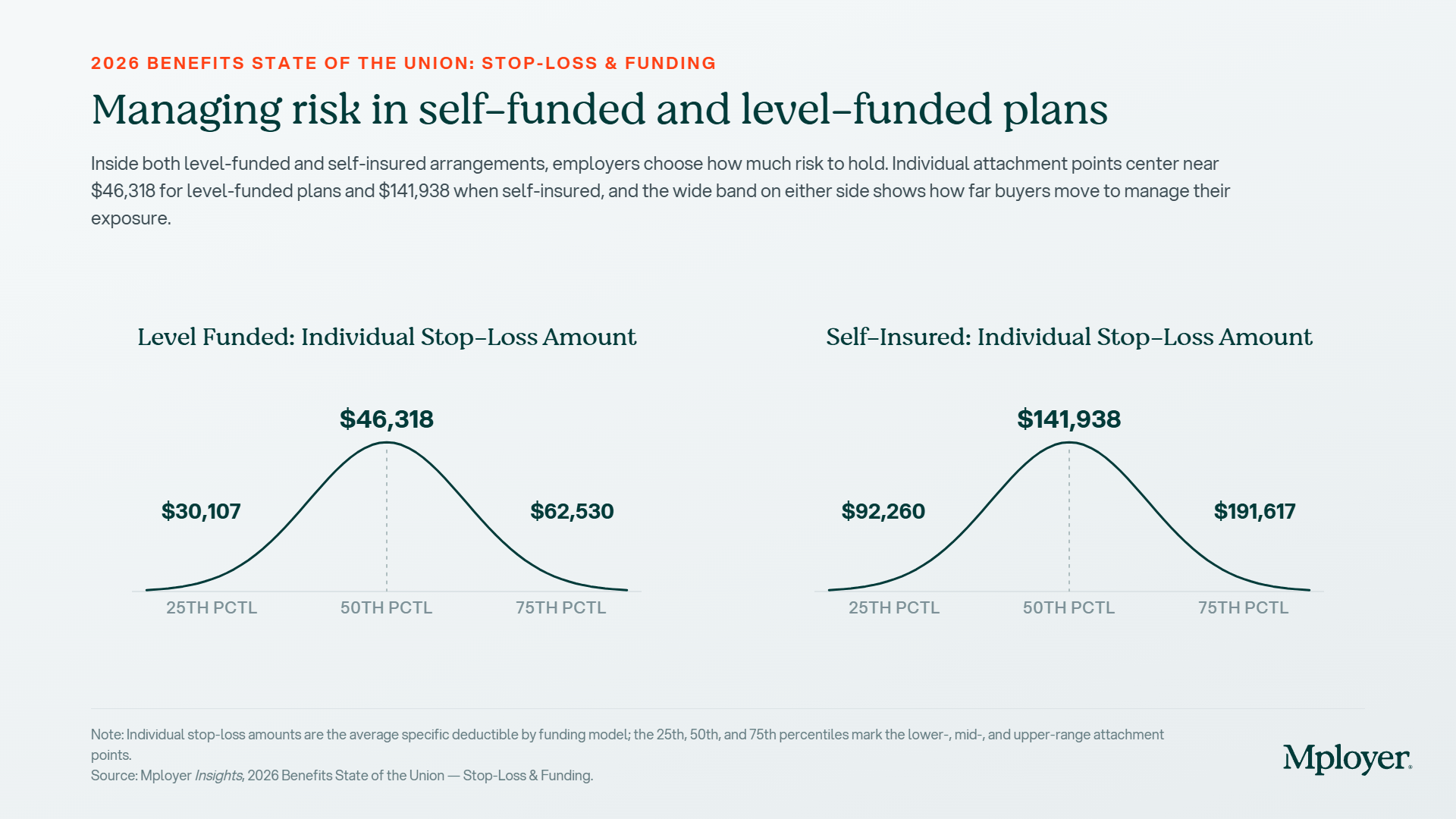

The average individual stop-loss deductible for level-funded plans is $46,318, meaning the employer’s claims fund absorbs the first $46,318 of any individual’s claims before stop-loss coverage kicks in. Level-funded plans give employers their first look at actual claims data, something a fully insured employer never sees, which is often the most valuable outcome of making the switch, independent of any refund.

Self-Funded (Self-Insured)

In a self-funded arrangement, the employer pays claims directly as they are incurred rather than paying a fixed premium. A third-party administrator (TPA) or carrier handles plan administration (network access, claims processing, member services),while the employer retains the financial risk. Stop-loss insurance caps the employer’s exposure on catastrophic individual claims and, optionally, on aggregate plan-wide costs.

The average individual stop-loss deductible for self-insured plans is $141,938, three times the level-funded equivalent, reflecting the higher risk tolerance required to make self-funding economically viable. PMPM costs in self-funded plans are highly variable month to month because costs track actual claims rather than a fixed premium. In a good year, a self-funded employer pays less than they would have under a fully insured arrangement. In a bad year, one with high utilization or a catastrophic claim, stop-loss coverage is what prevents the plan from becoming a financial crisis.

Key Terms Every CHRO and CFO Should Know

Benefits funding conversations move quickly into jargon. These are the terms that matter most:

- PMPM (Per Member Per Month): The standard unit for measuring health plan costs. Total annual plan cost divided by total member months. Used to compare costs across plans, funding structures, and years. A fully insured employer often doesn’t know their PMPM, a self-funded employer tracks it monthly.

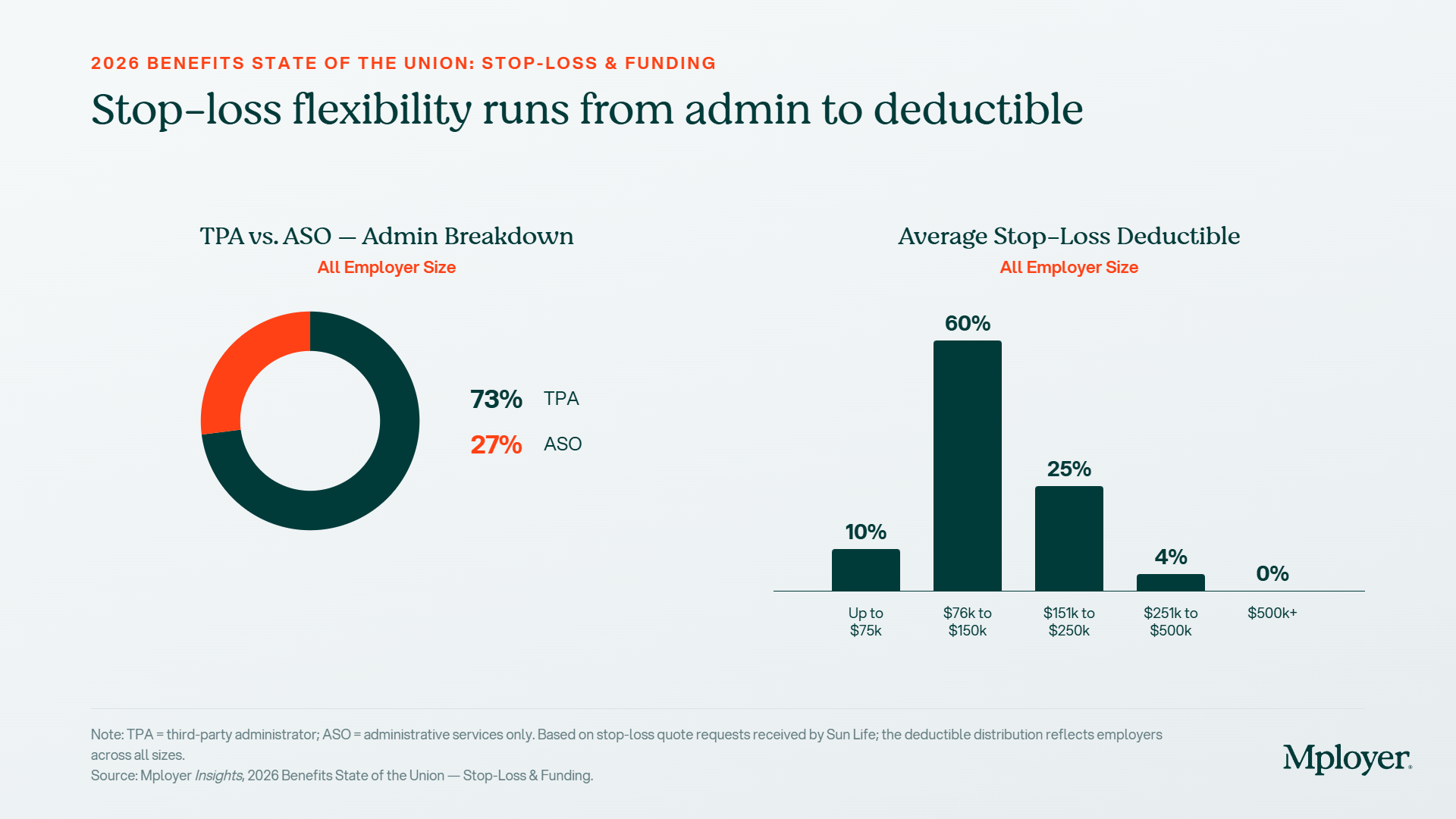

- Stop-Loss Insurance: Insurance purchased by self-funded and level-funded employers to cap their claims exposure. Specific stop-loss covers individual catastrophic claims above a deductible. Aggregate stop-loss covers total plan costs that exceed a set percentage of expected claims (typically 120–125%). Nationally, 92% of self-funded employers carry specific-only stop-loss; 8% carry both specific and aggregate.

- Specific Stop-Loss Deductible: The per-person threshold above which the stop-loss carrier begins reimbursing claims. Level-funded average: $46,318. Self-insured average: $141,938. Setting this number too high exposes the employer to more risk per claim; too low raises the stop-loss premium.

- TPA (Third-Party Administrator): An independent organization that administers a self-funded plan, processing claims, managing networks, and handling compliance. 73% of self-funded employers use a TPA. TPAs are carrier-agnostic and give employers more flexibility in how they assemble their plan.

- ASO (Administrative Services Only): An arrangement where a major carrier (UnitedHealthcare, Aetna, Cigna, BCBS) administers the plan while the employer retains financial risk. 27% of self-funded employers use ASO. Provides access to the carrier’s national network and integrated services.

- Run-Out Claims: Claims incurred before a plan year ends but submitted after. A critical concept when switching funding structures, an employer moving from fully insured to self-funded must account for run-out liability from the prior plan year.

- Lasering: A stop-loss carrier practice of excluding a specific high-cost individual from coverage, or charging a higher deductible for them, at renewal. Common for known catastrophic claimants. Employers should understand their stop-loss carrier’s lasering policy before selecting a deductible.

- Aggregate Risk Corridor: The band above expected claims before aggregate stop-loss kicks in, typically 120–125% of projected costs. An employer with $10M in expected claims and a 1.22 corridor absorbs the first $12.2M before aggregate coverage begins.

Plan Administration: TPA vs. ASO and How Vendors Fit Together

One of the most underappreciated aspects of moving to a self-funded model is that it separates plan administration from plan financing. Under a fully insured arrangement, the carrier does both. Under a self-funded arrangement, the employer can assemble a best-of-breed stack: choosing a TPA for administration, a separate stop-loss carrier for risk protection, a PBM for pharmacy, and a network rental arrangement for provider access. That modularity is both the primary advantage and the primary complexity of self-funding.

Third-Party Administrators (TPAs)

TPAs administer the day-to-day operations of a self-funded plan without carrying any of the insurance risk. They process claims, manage member ID cards, handle appeals, provide reporting, and ensure compliance. Because they are carrier-agnostic, employers using a TPA can select their network, stop-loss carrier, and PBM independently. Key TPA vendors in the market include:

- Imagine360 — self-funded and reference-based pricing specialist; strong mid-market focus

- Allied Administrators — independent TPA with regional strength and flexible plan design

- Trustmark — TPA with integrated level-funded and self-funded products

- Benefit Administration Company (BAC) — mid-market TPA with stop-loss relationships

- Sun Life — major stop-loss carrier that also provides TPA services and data analytics

Administrative Services Only (ASO) Carriers

Under an ASO arrangement, the employer accesses a major carrier’s infrastructure — their provider network, claims processing systems, and member services, while self-funding the actual claims. The primary advantage is network breadth: UnitedHealthcare, Aetna, Cigna, and the Blue Cross Blue Shield plans have national networks that most TPAs cannot replicate. The tradeoff is less plan design flexibility and, typically, less direct access to claims data. ASO is the most common path for large employers who want the benefits of self-funding without building an entirely independent plan infrastructure.

Carving Out Vendors: Where Employers Have the Most Leverage

One of the most powerful moves available to self-funded and level-funded employers is selectively replacing the default vendor stack with purpose-built alternatives. The most common carve-outs:

- PBM Carve-Out: Most ASO carriers bundle their own PBM (UHC uses OptumRx, Aetna uses CVS Caremark, Cigna uses Express Scripts). Employers can carve out the PBM and contract directly with an independent pharmacy benefit manager, often achieving better rebate pass-through and lower net drug costs. Employers with 500+ covered lives typically have the leverage to negotiate meaningfully. Independent PBMs like Capital Rx, Navitus, and SmithRx are built specifically for transparent, pass-through pricing models.

- Specialty Pharmacy Carve-Out: Specialty drug spend (oncology, biologics, GLP-1s) is the fastest-growing cost component in most plans. Carving specialty pharmacy to a dedicated specialty PBM or white-bagging program, where drugs are dispensed through the employer’s preferred channel rather than a hospital pharmacy, can generate material savings on a small number of high-cost claimants.

- Centers of Excellence (COE) Carve-Out: For high-cost procedures like joint replacement, cardiac surgery, bariatric surgery, and oncology treatment, employers can steer members to designated high-quality, lower-cost providers. COE programs through vendors like Included Health, Transcarent, and the major carrier networks have demonstrated both quality improvements and cost reductions for self-funded employers.

- Mental Health / EAP Carve-Out: Traditional EAPs have low utilization and limited clinical depth. A growing number of self-funded employers are carving out behavioral health to dedicated platforms (i.e. Lyra Health, Spring Health, Headspace Health) that offer broader access and measurable utilization outcomes.

- Stop-Loss Carve-Out: ASO carriers often offer stop-loss as part of their package. Self-funded employers can go to market independently with stop-loss carriers (i.e. Sun Life, Tokio Marine HCC, Voya, Symetra) to find better rates, higher deductibles, or more favorable lasering terms.

Each carve-out adds administrative complexity and requires coordination between vendors. The benefit of a TPA is that it can serve as the integrating layer, managing data feeds, eligibility, and claims adjudication across a multi-vendor stack. For employers considering their first carve-out, the PBM is usually where the most immediate financial opportunity exists.

High-Cost Claimants and What the Stop-Loss Data Shows

For any self-funded or level-funded employer, understanding high-cost claimant dynamics is essential. A single member with a catastrophic diagnosis, a premature birth requiring NICU care, an oncology case requiring immunotherapy, or a rare disease requiring gene therapy, can represent more claims cost than dozens of average members combined.

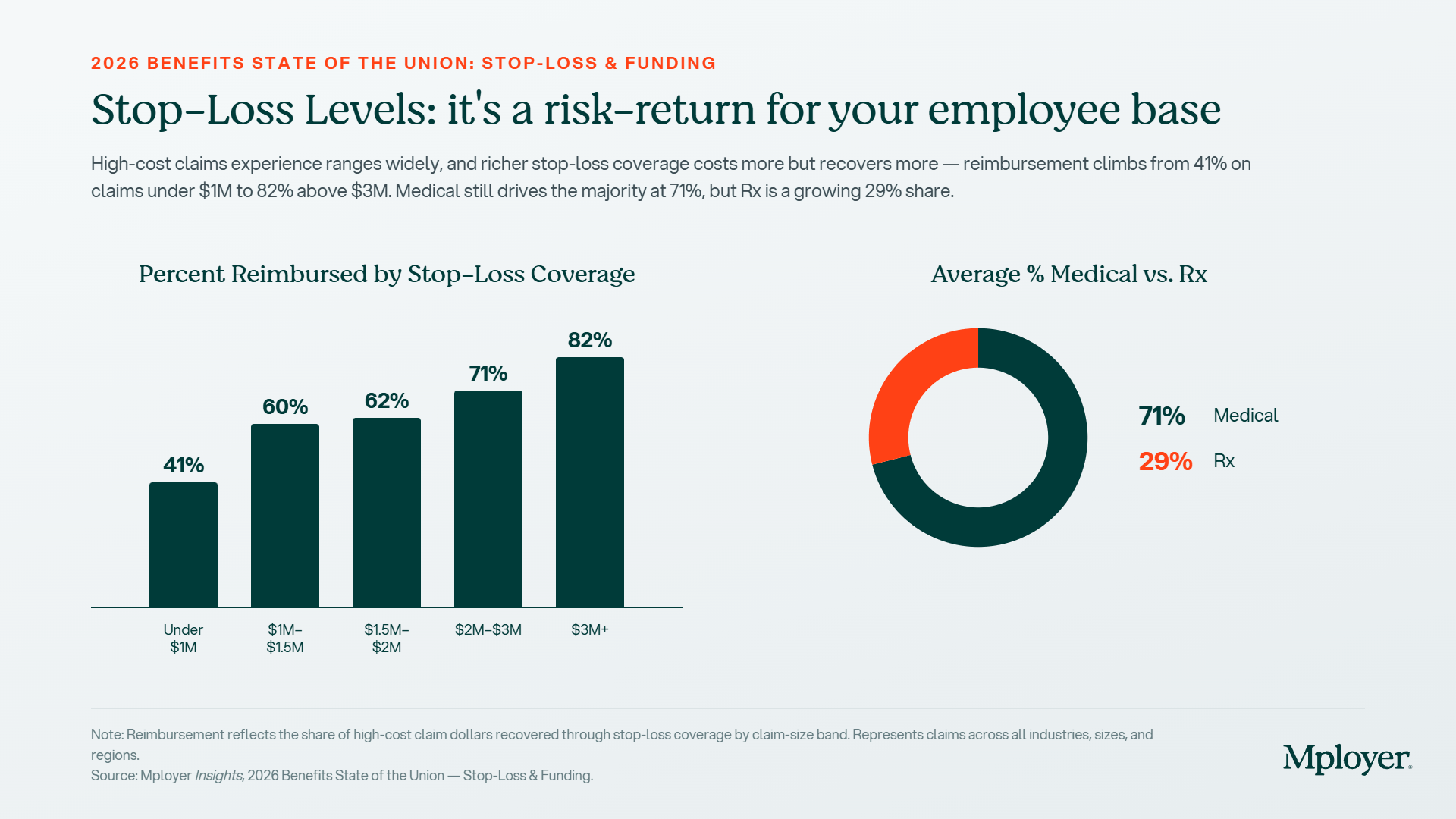

The stop-loss reimbursement data illustrates how the financial burden of large claims is distributed between employers and their stop-loss carriers:

- Claims under $1M: 41% reimbursed by stop-loss, employers absorb the majority

- Claims $1M–1.5M: 60% reimbursed, stop-loss begins to shoulder more

- Claims $1.5M–2M: 62% reimbursed

- Claims $2M–3M: 71% reimbursed

- Claims over $3M: 82% reimbursed, stop-loss is covering the vast majority

The practical implication: stop-loss coverage is most valuable at the extremes. Below $1M in total claims, the employer is absorbing nearly 60 cents of every dollar. Above $3M, the stop-loss carrier is covering 82%. Setting the right specific stop-loss deductible is therefore a meaningful financial decision, higher deductibles reduce stop-loss premiums but increase the employer’s per-incident exposure.

The composition of those high-cost claims matters too. Nationally, 71% of high-cost claim dollars are medical and 29% are pharmacy. That pharmacy share is rising. Specialty drugs, like particularly oncology therapies, biologics, and increasingly GLP-1 medications, are driving the Rx portion higher year over year. For self-funded employers, a specialty drug claim for a single member can now approach or exceed the average $141,938 stop-loss deductible in a single plan year. This is why formulary design, specialty pharmacy strategy, and stop-loss adequacy are increasingly interconnected decisions rather than separate ones.

What to Consider If You Are Fully Insured and Want to Understand Your Options

Moving from fully insured to level-funded or self-funded is not a decision to make lightly. It requires the employer, their CFO, their CHRO, and their broker or consultant to answer a set of questions honestly before modeling the economics:

- Size: Do you have enough covered lives to make the model actuarially viable? Level-funded is generally accessible at 25–50+ lives. True self-funding typically requires 100+ covered lives to carry meaningful claims risk, and 200+ before the economics are compelling without level-funded guardrails.

- Cash flow: Can your organization absorb monthly claims variance? Self-funded plans pay claims as incurred; a bad month is a real cash event, not just a future premium increase. Stop-loss reimbursement typically runs 30–90 days after the claim is paid, creating a temporary cash flow gap.

- Risk tolerance: Is your leadership prepared for year-to-year cost variability? Self-funding can produce meaningful savings in good years and meaningful overruns in bad ones. The multi-year economics almost always favor self-funding at sufficient scale, but the path is not smooth.

- Administrative capacity: Self-funded plans require more active management, including stop-loss renewals, TPA oversight, claims audits, and compliance filings. Your broker or consultant needs to have genuine self-funded expertise, not just familiarity with the concept.

- Data readiness: The primary non-financial benefit of self-funding is access to your own claims data. Are you prepared to actually use that data to make plan design decisions? Employers who self-fund without using their claims data are paying for a capability they’re not capturing.

- Run-out liability: When leaving a fully insured arrangement, the employer is responsible for claims incurred during the fully insured period but submitted afterward. This run-out must be accounted for in the financial model, it is often the surprise that derails first-year self-funded economics for employers who didn’t plan for it.

If the answers to these questions are uncertain, level-funded is almost always the right first step. It provides the refund upside and data transparency of self-funding with the fixed monthly cost and administrative simplicity of fully insured. For many employers in the 50–250 life range, level-funded is not a stepping stone, it is the right permanent answer.

The Point Is Not Which Model; It’s Whether You Know What You’re In

The most important outcome of understanding plan funding is not deciding to switch models. It is being able to have an informed conversation with your broker, your CFO, and your board about what you’re paying, what you’re getting, and what the alternatives look like.

An employer who has been fully insured for ten years and has never modeled a level-funded alternative does not know what that decision is costing them. An employer who is self-funded but has never analyzed their claims data does not know what that structure is worth. In both cases, the answer starts with a benchmark, knowing where your plan sits relative to employers who actually look like you.

Mployer’s benefits rating evaluates plan funding structure, stop-loss levels, and PMPM costs as part of the Medical pillar score, so employers can see not just what they’re paying, but how that compares to their custom cohort.

Curious to see how your benefits compare?

Or Schedule a Demo to get started.

Sources

Mployer 2025 and 2026 Employee Benefit Plan Design Study, covering 50,000+ employer plans.

Stop-Loss Snapshot: Sun Life stop-loss quote requests, all size average. Segmented by employer size.

KFF 2025 Employer Health Benefits Survey. Average annual premiums: $9,325 single / $26,993 family.

U.S. Department of Labor: self-funding adoption by employer size. 27% of firms 100–199 employees; 90%+ of firms 5,000+ employees.

Mercer 2025 National Survey of Employer-Sponsored Health Plans: average total plan cost $17,496 PEPY; projected to exceed $18,500 in 2026.

.jpg)

June's product updates are here, and there's a lot to be excited about. We're continuing to build on the foundation we've established across Catalyst and Insights benchmarking, with this month's updates focused on giving users more precision in how they search, prospect, and manage data.

On the Catalyst side, that means expanded AI assistant capabilities, more flexible export controls, and deeper CRM customization. For benchmarking, we've added AI-powered recommendations and made meaningful improvements to the report experience, including how you access completed reports and how data flows through the submission wizard.

Read on for the full details.

Catalyst

- Proximity-Based Geographic Search — The AI assistant now supports radius-based company searches around a city, so territory prospecting works the way territories actually do — not just by state, city, or zip.

- Product Line Gap Queries — Ask the AI assistant which product lines — Stop Loss, EAP, Voluntary, TPA — an employer has or is missing. Cross-sell identification now happens in a conversation, not a spreadsheet.

- Headcount Milestone Flags — The AI assistant can surface employers who've recently crossed key thresholds: 50, 100, 500 employees. Growth signals and compliance triggers, surfaced automatically.

- Flexible Export Range Selection — When exporting data, users can now choose the current page, a page range, or a specific record count. Providing precise control without bumping into system limits.

- Experience Mod Data on Account View — Experience Modification data now appears directly on the Company Overview and Commercial P&C tab, so risk context is right there when you need it.

- Custom CRM Field Mapping — Account admins can now map platform fields to custom CRM fields, including custom schemas. Providing full control over how data flows in without overwriting existing records.

- Retirement Search: Total Assets Filter — The Retirement Search Assets filter now filters on Total Assets.

Insights+

- AI-Powered Recommendations in Insights+ Users can now access AI-generated recommendations directly within Insights+. The new recommendations tool surfaces actionable guidance across four categories. Highest Impact, Cost Strategy, Coverage Gaps, and Underwriter Notes, giving users a faster path from report data to next steps.

- Completion Email Links to HTML Report — When your report is ready, the notification email now links directly to the interactive HTML report including Mployer AI and all report tools, instead of a PDF download.

- Redesigned Chart Layout — Plan Score and Cohort Market Data sections are now clearly differentiated, and Dental and Vision pages consolidate their left-side tables. Easier to read, faster to interpret.

- Report Opens Without Losing Your Place — Clicking a company name in the Request History Grid now opens the HTML report in a new tab, so your search state stays exactly where you left it.

- Rate Availability Edits No Longer Clear Rate Data — Adjusting Rate Availability selections mid-wizard no longer wipes Medical, Dental, or Vision rate and contribution data previously entered. No more lost work.

- Age-Banded Entry Hidden When Not Applicable — When 'Use employee contributions only' is selected, Age-Banded rate entry is no longer shown — cleaner form, fewer distractions.

That's a wrap! Stay tuned for what's coming next month.

.jpg)

The Tax Advantage Most Employers Are Leaving on the Table

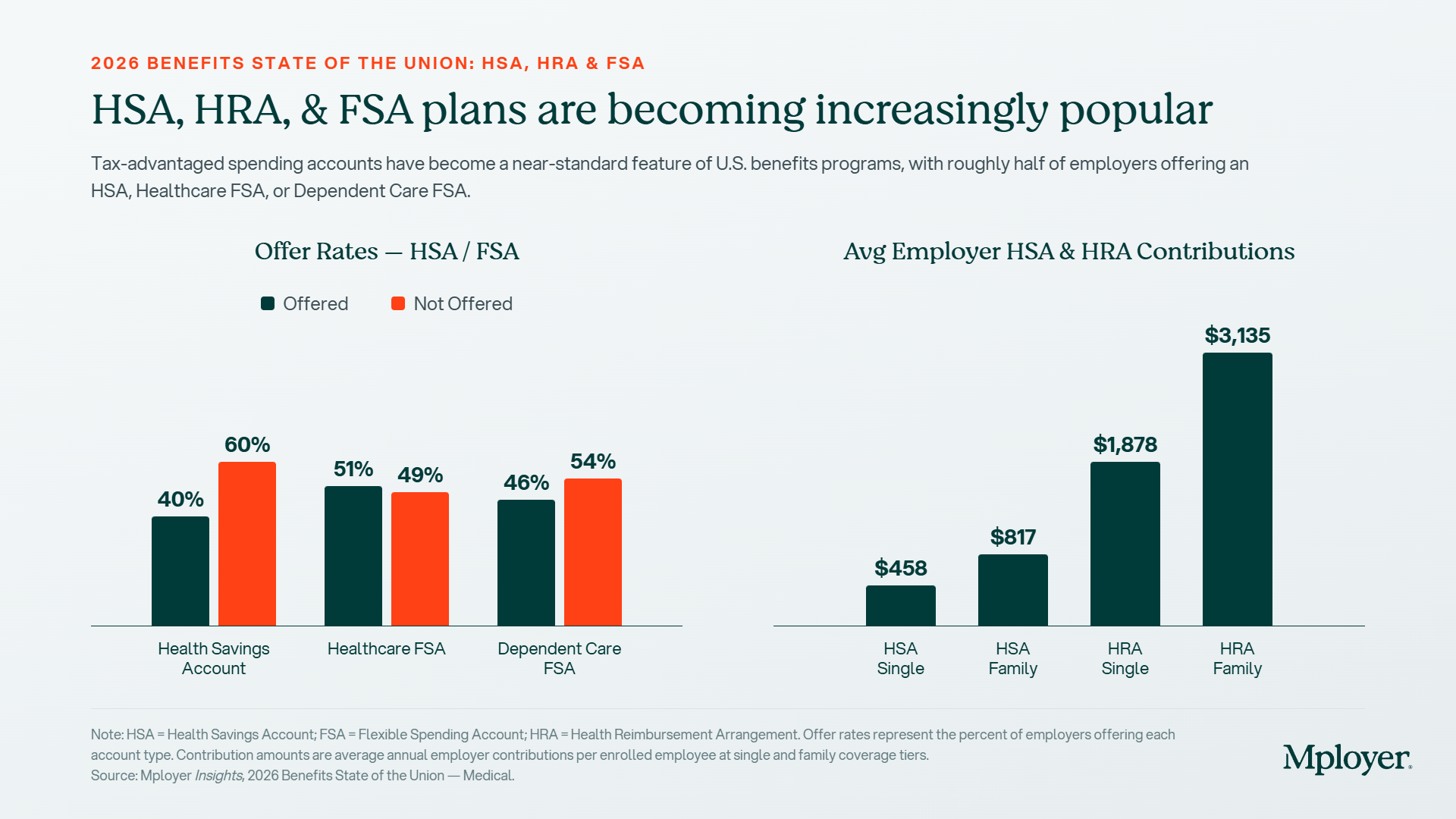

There are very few mechanisms in the U.S. benefits system that are truly triple tax-advantaged. The Health Savings Account is one of them. Contributions go in pre-tax, grow tax-free, and come out tax-free when used for qualified medical expenses. For employers, an HSA is also a funding tool: a way to offset the cost impact of pairing employees with a high-deductible health plan while creating real, measurable value that employees can carry with them.

And yet, only 40% of employers currently offer an HSA. That means six out of ten are not providing access to one of the most tax-efficient benefits tools available; in many cases because they’ve defaulted to a PPO or HMO structure without modeling what a consumer-directed health plan paired with meaningful employer HSA funding would look like competitively.

This is not a promotion for HSAs and HRAs, the only goal is to provide a more detailed understanding of how they work and their adoption to date. This covers what HSAs and related cost-sharing vehicles actually are, how they interact with plan design, what employers are contributing nationally, the key vendors in the space, and what separates employers who use these tools strategically from those who don’t.

HSA, HRA, FSA: What Each One Actually Is

These three accounts are often grouped together but they work very differently. Understanding the distinctions matters before designing a benefits strategy around any of them.

Health Savings Account (HSA)

An HSA is an individually owned, portable savings account available only to employees enrolled in a qualified High-Deductible Health Plan (HDHP). Contributions can come from the employer, the employee, or both, up to IRS annual limits ($4,400 single / $8,750 family for 2026). Funds roll over year to year, can be invested, and remain with the employee if they leave. The triple tax advantage (pre-tax in, tax-free growth, tax-free out for qualified expenses) makes this the most valuable account structure of the three.

Key rules to know:

- Must be paired with an IRS-qualified HDHP (2026 minimums: $1,700 single / $3,400 family deductible; OOP maximums: $8,500 single / $17,000 family)

- Employee cannot be enrolled in Medicare, claimed as a dependent, or have other disqualifying coverage

- Unused funds roll over indefinitely, there is no use-it-or-lose-it provision

- After age 65, funds can be withdrawn for any purpose (ordinary income tax applies, like a 401k)

- Employer contributions are not subject to payroll tax, a savings of ~7.65% on every dollar contributed

- Catch-up contribution for employees age 55+: additional $1,000 per year (unchanged for 2026)

Health Reimbursement Arrangement (HRA)

An HRA is employer-owned and employer-funded. Unlike an HSA, the employee never receives or holds the funds, rather the employer reimburses eligible expenses up to a set annual limit. Unused balances can be carried over at the employer’s discretion or forfeited at year-end. Because the employer retains unused funds, HRAs are particularly attractive for employers who want to offer meaningful financial support to employees while limiting their actual cash outlay to claims incurred.

Key rules to know:

- Employer-funded only, employees cannot contribute

- Can be paired with any plan type, including PPO and HMO (unlike HSA)

- Employer decides what qualifies as a reimbursable expense

- ICHRA (Individual Coverage HRA) allows employers to reimburse individual market premiums, a growing alternative to group coverage

- Forfeitures return to the employer, making this a lower actual-cost vehicle than the stated contribution amount

- Excepted Benefit HRA (EBHRA) limit for 2026: $2,200 per year (up from $2,150 in 2025)

Flexible Spending Account (FSA)

An FSA is an employer-sponsored, employee-funded account for pre-tax healthcare or dependent care expenses. The Healthcare FSA is offered by 51% of employers and is the most widely available of the three accounts. However, the classic “use it or lose it” rule applies: unused funds are generally forfeited at year-end, though employers may allow a grace period or a limited rollover. FSAs can be paired with PPO and HMO plans but cannot be used alongside a standard HSA.

Key rules to know:

- Employee-funded via pre-tax payroll deductions (employers may also contribute)

- Healthcare FSA 2026 employee contribution limit: $3,300 per employee (unchanged from 2025)

- Dependent Care FSA is separate and covers childcare and elder care (46% of employers offer this)

- Use-it-or-lose-it: forfeitures stay with the employer unless a rollover or grace period is offered

- Limited Purpose FSA can be used alongside an HSA for dental and vision expenses only

How Plan Design and HSA Eligibility Connect

The most important design constraint for employers to understand: an HSA is only available to employees enrolled in a qualified HDHP. That connection makes HDHP plan design decisions and HSA funding strategy inseparable.

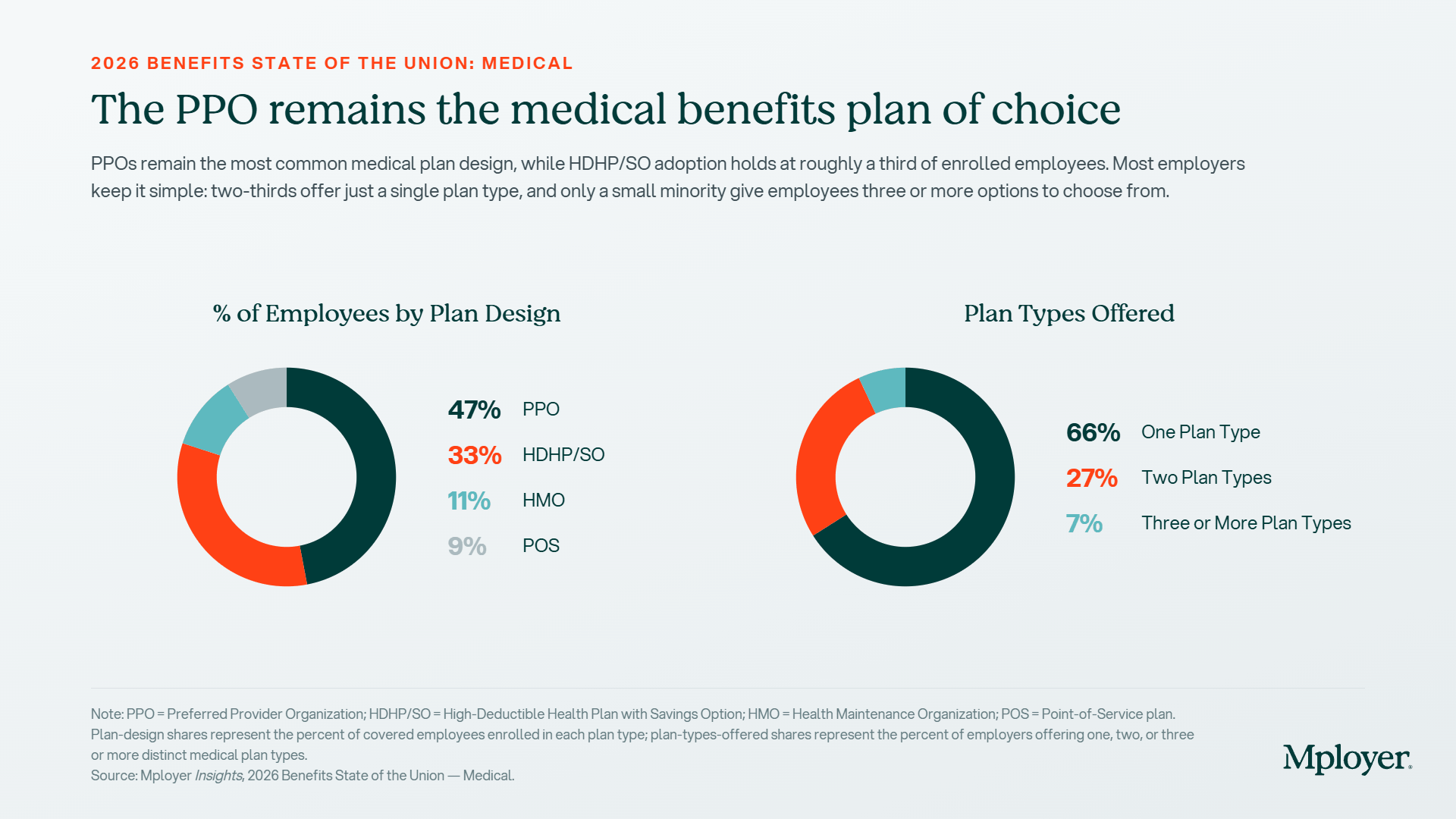

Currently, 33% of employees nationally are enrolled in an HDHP/SO plan, compared to 47% in a PPO. HDHP deductibles average $3,460 for single coverage and $8,273 for family, meaningfully higher than PPO averages of $1,857 single and $1,638 family aggregate. For 2026, the IRS minimum HDHP deductible is $1,700 for single coverage and $3,400 for family, with an out-of-pocket maximum of $8,500 single / $17,000 family. That deductible gap is the core employee concern with HDHPs, and it’s precisely where employer HSA contributions come in.

When an employer pairs an HDHP with a meaningful HSA contribution, they are effectively offsetting a portion of the employee’s deductible exposure upfront, making the high-deductible plan significantly more attractive. An employer contributing $458 toward a single employee’s HSA reduces the net deductible that employee faces from $3,460 to roughly $3,000. An employer contributing nothing leaves that gap entirely to the employee, making the HDHP structurally punishing compared to a PPO.

A PPO does not qualify employees for HSA contributions. PPO plans can be paired with an HRA (employer-funded only) or a Healthcare FSA (employee-funded, pre-tax). This is an important distinction for employers offering multiple plan types, the account strategy differs depending on which plan the employee selects.

What Employers Are Actually Contributing: The National Benchmarks

The gap between HSA and HRA employer contribution levels is striking. According to Mployer’s plan data covering 50,000+ employers:

- Average employer HSA contribution: $458 for single coverage / $817 for family coverage

- Average employer HRA contribution: $1,878 for single coverage / $3,135 for family coverage

- Only 40% of employers offer an HSA at all, 60% do not

- Healthcare FSA offer rate: 51%

- Dependent Care FSA offer rate: 46%

The HRA contribution averages are substantially higher than HSA averages for a structural reason: HRAs are employer-owned accounts, and employers have full control over what is actually paid out. Because forfeitures return to the employer, the stated contribution amount overstates the actual cost. Employers using HRAs strategically understand that the funded amount and the realized cost are different numbers and that gap can be significant depending on utilization patterns.

For employers offering HSAs, the question is not just whether to contribute, but how much. An HSA employer contribution of $0 foregoes payroll tax savings on every dollar that could have been contributed, and removes a key differentiator for employers whose HDHP deductibles are above market. The 2026 IRS maximum contribution is $4,400 for single coverage and $8,750 for family; meaning the average employer contribution of $458 single represents just 10% of what employees could potentially receive tax-free.

Copays, Cost-Sharing, and How They Interact with Account-Based Plans

One of the most common points of confusion for employees, and plan sponsors, is how copays work in the context of HDHPs and HSAs.

In a traditional PPO or HMO, employees typically pay a flat copay at the point of service: $27 for a PCP visit under a PPO, $26 under an HMO, $29 under a POS plan (national averages from Mployer’s data). These copays do not count toward the deductible in most cases and take effect immediately regardless of whether the deductible has been met.

In a true HDHP, IRS rules generally prohibit first-dollar coverage, meaning copays cannot apply before the deductible is met (with limited exceptions for preventive care). The employee pays the full negotiated rate for services until the deductible is satisfied, at which point coinsurance or copays kick in. This is a fundamentally different employee experience, and one that drives the perception that HDHPs are always worse for employees. The reality depends on the employer’s HSA funding strategy and where the employee lands on the utilization curve.

Employer decisions about hospital cost-sharing further shape this picture. For inpatient hospital services under HDHP plans, 70% of employers use copayment structures; for outpatient, 74% use copayments. Under PPO plans, hospital cost-sharing is more evenly split between copayments and coinsurance. These structural choices, combined with deductible levels and HSA funding, determine the real cost experience for employees across plan types.

The Vendor Landscape: Who Administers These Accounts

Setting up and administering HSAs, HRAs, and FSAs requires a third-party administrator. The vendor landscape is well-developed but fragmented, and the right choice depends on employer size, plan complexity, and whether investment options are a priority.

HSA Custodians

- Fidelity: the largest HSA provider by assets; no account fees, strong investment options, integrates with payroll

- HealthEquity: major HSA custodian with employer-facing administration tools and HDHP carrier partnerships

- HSA Bank: bank-based custodian offering FDIC-insured accounts and investment options through TD Ameritrade

- Optum Financial: UnitedHealth-owned platform with strong integration into UHC medical plans

- WEX Health: multi-account platform covering HSA, HRA, and FSA administration in one system

HRA Administrators

- PeopleKeep: specializes in ICHRA and QSEHRA for small and mid-size employers; strong compliance support

- Take Command Health: ICHRA-focused platform with employee-facing marketplace integration

- Businessolver: enterprise benefits administration platform with integrated HRA management

- Most major TPAs (Benefitfocus, bswift) offer HRA administration as part of broader benefits admin

FSA Administrators

- WEX: one of the largest FSA administrators; covers Healthcare FSA, Dependent Care FSA, and transit accounts

- Flores & Associates: independent FSA/HRA administrator with a strong employer service model

- Ameriflex: mid-market focused FSA/HRA/COBRA administrator with a clean debit card experience

- PayFlex (Aetna): integrated with Aetna medical plans; common in employer groups already on Aetna

For employers setting up an account-based plan for the first time, the most common path is to start with the HSA or FSA administrator recommended by their medical carrier or broker. While convenient, this is not always the lowest-cost or highest-value option. Employers with self-funded plans or significant HSA-eligible populations should evaluate custodians independently, particularly investment options, account fees, and payroll integration.

How the Strategy Is Evolving

The account-based benefits landscape has expanded meaningfully since 2020. The introduction of ICHRAs (Individual Coverage HRAs) gives employers a new tool: instead of offering a group health plan, they can provide a defined dollar contribution that employees use to purchase individual market coverage. For distributed workforces, part-time heavy employers, or organizations in markets where group plan design is always a compromise, ICHRAs are increasingly worth modeling.

HSAs are also increasingly being positioned as a retirement health savings vehicle. Employees who contribute to an HSA and invest the balance, rather than spending it down each year, can accumulate a meaningful reserve for post-retirement healthcare costs. Fidelity estimates that a 65-year-old couple retiring today will need approximately $315,000 to cover healthcare costs in retirement. An HSA is one of the only accounts that can address that liability with pre-tax dollars.

IRS contribution limits for 2026: $4,400 for self-only HDHP coverage and $8,750 for family coverage, with an additional $1,000 catch-up contribution for those age 55 and older. HDHP minimum deductibles are $1,700 single / $3,400 family, with out-of-pocket maximums of $8,500 single / $17,000 family. Employers who set their HSA contribution strategy once and don’t revisit it annually may be leaving employees with a funding gap as limits increase each year.

Know How Your HSA Strategy Compares

Most employers know what they contribute to an HSA. Few know how that contribution compares to what their peers (same industry, location, and size) are contributing. An employer contributing $200 to a single employee’s HSA may feel like they’re offering something meaningful. Against a cohort where the average is $458, they’re below market in a category employees increasingly compare.

Mployer’s benefits rating evaluates HSA and HRA funding levels as part of the Medical pillar score (alongside deductibles, premiums, and plan design) to show employers exactly where their cost-sharing strategy sits relative to their custom cohort.

Curious to see how your benefits compare?

Or Schedule a Demo to get started.

Sources

Mployer 2025 and 2026 Employee Benefit Plan Design Study, covering 50,000+ employer plans.

IRS Revenue Procedure 2025-19: 2026 HSA contribution limits ($4,400 single / $8,750 family), HDHP minimum deductibles ($1,700 single / $3,400 family), and HDHP out-of-pocket maximums ($8,500 single / $17,000 family).

Fidelity Investments Retiree Health Care Cost Estimate, 2025.

.svg)

.svg)

.svg)

.svg)